EXPOSED: The 'One-Bill' Loophole Canadian Banks Are Trying to Hide From Homeowners

A strange but highly effective financial loophole allows everyday Canadians to package their high-interest credit cards into a single, aggressively low monthly payment, entirely bypassing traditional bank rates.

Last month, Canadian household debt hit a grim milestone, reaching a staggering 180% of disposable income. With the Bank of Canada holding interest rates at punishing highs, the cost of living has spiraled out of control. Grocery bills in Ontario and British Columbia have nearly doubled, gas prices remain volatile, and impending mortgage renewals are acting as a ticking time bomb for middle-class families.

For millions of Canadian homeowners, the only way to keep the lights on and food on the table has been to rely on credit cards. But as balances creep up, the "Minimum Payment Trap" snaps shut. When you are paying 22.99% interest on a piece of plastic, a $15,000 balance can take decades to pay off, costing tens of thousands in pure interest profit for the big banks.

The Homeowner's Nightmare

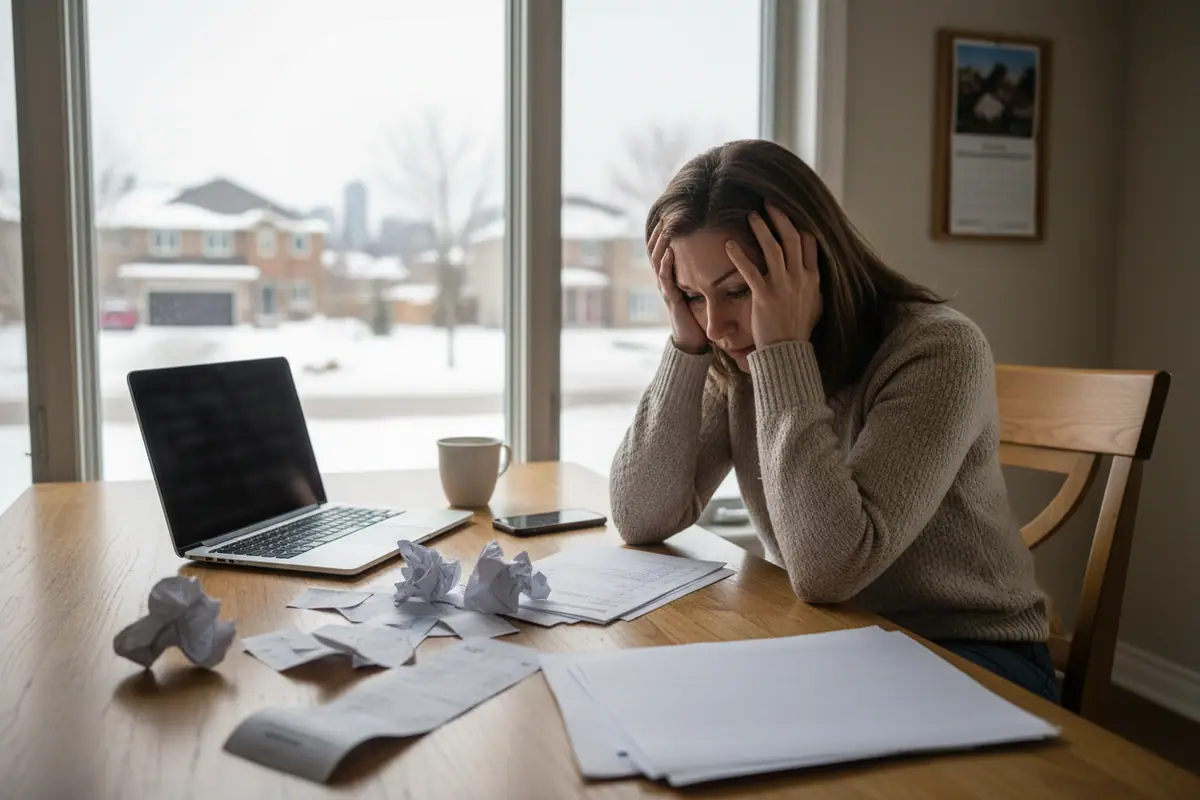

Meet Mark Reynolds, a 44-year-old homeowner from Calgary, Alberta. Over the past three years, Mark watched his financial stability evaporate. Between a sudden roof repair, rising property taxes, and the sheer cost of feeding his family of four, Mark accumulated $34,000 in debt spread across three different credit cards.

"I was drowning," Mark told our editorial team, his voice heavy with exhaustion. "Every month, I was paying over $900 just in minimum payments. When I looked at my statements, maybe $40 of that was actually going toward the principal balance. The rest was just pure profit for the banks. I was seriously considering putting a 'For Sale' sign on my front lawn just to escape the debt."

Mark's situation is not unique. Across the country, hardworking homeowners are quietly suffocating under revolving credit card debt, terrified that one missed payment will trigger a cascade of penalties, collection calls, and ultimately, the loss of their homes.

A Late-Night Discovery

Mark thought bankruptcy or selling his home were his only two options. That was until a neighborhood barbecue changed everything. Mark confided in a former mortgage broker who had recently retired from one of Canada's "Big Five" banks. The retired banker looked around, lowered his voice, and told Mark about a little-known financial mechanism.

It wasn't a standard bank loan, a risky second mortgage, or a Home Equity Line of Credit (HELOC). The ex-banker explained that there was a legal loophole designed to bypass the traditional banking system entirely. He called it Canada Debt Consolidation.

According to the retired insider, the banks absolutely despise this mechanism. Why? Because the 'One-Bill' loophole forces creditors to the negotiating table, stripping away compounding interest and packaging multiple chaotic debts into one single, aggressively low monthly payment. It effectively cuts off the banks' most lucrative revenue stream: middle-class interest payments.

The Skeptical Investigation

When Mark first contacted our financial news desk to share his story, my journalistic alarm bells immediately went off. I have spent the last twelve years investigating predatory lending, payday loan scams, and financial fraud across Toronto and Vancouver. Whenever someone mentions a "loophole" to erase debt, I assume it is a scam designed to steal upfront fees from vulnerable people.

I assumed Canada Debt Consolidation was just another predatory trap disguised as a lifeline.

To find out the truth, our editorial board decided we couldn't just take Mark's word for it. We needed to run a covert, rigorous investigation. We decided to put this mechanism to the ultimate test. We asked Sarah, a junior editor on our staff who lives in Mississauga, to volunteer. Sarah is a homeowner who was quietly battling $26,500 in high-interest debt across a major bank Visa, a retail Mastercard, and a hardware store credit card. Her combined minimum payments were choking her monthly budget.

We instructed Sarah to apply for the Canada Debt Consolidation program, documenting every single step of the process to see if the 'One-Bill' loophole was a legitimate financial rescue plan, or just smoke and mirrors.

Day 1

Sarah submitted her initial assessment through the official online portal. The process took less than three minutes. As a skeptic, I warned her to watch out for hidden upfront fees or a hard credit check that would instantly tank her credit score. Surprisingly, neither happened. The system simply asked for a rough estimate of her total unsecured debt and her province of residence to verify her eligibility under local financial regulations.

Day 3

Sarah received a phone call from an assigned financial representative. I sat in on the call, ready to interrupt if it turned into a high-pressure sales pitch. Instead, the representative was strictly factual. They explained exactly how the 'One-Bill' mechanism worked. They wouldn't be lending Sarah more money to pay off her old money. Instead, they would use the Canada Debt Consolidation framework to intervene directly with her credit card companies, stopping the compounding interest in its tracks.

Day 7

This was the turning point. Sarah received her finalized consolidation agreement. The results were difficult to argue with. Her $26,500 debt, previously bleeding her dry at an average interest rate of 21.5%, was frozen. The harassing late notices from her retail card stopped immediately. All three of her chaotic, high-interest bills were packaged into a single monthly payment. Best of all, that new 'One-Bill' payment was a staggering 55% lower than the combined minimum payments she had been struggling to pay just a week prior.

The transformation we witnessed in our colleague was nothing short of profound. Instead of losing sleep over compounding interest and dreading the trip to the mailbox, Sarah is finally putting money back into her family's savings account. The crushing weight of the "Minimum Payment Trap" has been lifted. Last weekend, instead of picking up a grueling overtime shift just to cover bank fees, she booked a modest, stress-free trip to Banff with her husband—a luxury they hadn't been able to afford in over four years.

Our investigation confirmed what the retired banker had told Mark: the big Canadian banks are quietly lobbying to restrict access to this exact type of relief. Every time a homeowner utilizes this loophole, the banks lose out on thousands of dollars in projected interest revenue. They would much rather you keep paying 22% interest for the next twenty years, or force you to leverage the hard-earned equity in your home through a high-rate HELOC.

As economic pressures continue to mount and inflation squeezes the middle class, mechanisms like this are becoming rare lifelines. The Canada Debt Consolidation framework is currently available to homeowners carrying significant unsecured balances, but financial experts warn that as bank lobbying intensifies, the eligibility windows for these aggressive consolidation programs may begin to narrow.

If you are a Canadian homeowner carrying high-interest credit card balances, personal loans, or retail debt, ignoring the problem will only result in thousands of dollars lost to bank profits. Taking a few minutes to verify your eligibility for the 'One-Bill' loophole could be the single most important financial decision you make this year.

Bypasses Traditional Interest Rates

Immediately halts the devastating 20%+ compounding interest charged by major credit card companies.

The 'One-Bill' Advantage

Merges multiple chaotic, high-stress bills into one single, aggressively lower monthly payment.

Protects Your Home Equity

Provides severe debt relief without requiring you to take out a risky second mortgage or borrow against your home.

Stops Creditor Harassment

Legally freezes collection calls and prevents the accumulation of endless late penalties.

Utilizes Proven Frameworks

Operates under the established Canada Debt Consolidation mechanism to ensure full legal compliance and consumer protection.

FAQ

Is this just a second mortgage or a HELOC?

No. This is a critical distinction. The 'One-Bill' mechanism does not require you to borrow against the equity in your home. It deals exclusively with unsecured debt, meaning your property remains safe and untouched by this specific consolidation process.

Will utilizing this loophole ruin my credit score forever?

While any major debt restructuring has an initial impact on your credit report, resolving high-utilization debt is often the fastest way to financial recovery. Rebuilding your standing after clearing your balances is significantly faster and safer than carrying maxed-out, revolving credit card debt for decades.

How do I know if I qualify for Canada Debt Consolidation?

Qualification is primarily based on your total volume of unsecured debt (such as credit cards and personal loans) and your province of residence. It is designed specifically for Canadians who are struggling to make headway on their principal balances, rather than being strictly gatekept by perfect credit scores.

Comments

Is this just another consumer proposal scam? I've seen these ads everywhere on Facebook and I don't trust the big banks at all anymore.

@Robert H. I thought the exact same thing, but it's actually a completely different framework. I went through the process in March and my Scotia Visa is finally sitting at zero. It's legitimate.

Do I have to own a home to qualify for this? I rent an apartment out in Vancouver but I have about 18k in credit card debt from when I was in university.

How much are the upfront fees? Banks usually charge an arm and a leg just to look at your file for a consolidation loan. I can't afford to pay thousands just to get started.

@Sarah Jenkins There were zero upfront fees for me. The Canada Debt Consolidation process is built so they only get paid based on the debt they actually save you. Way cheaper than paying 22% interest to Mastercard every month.

How long does the approval take? I have a massive bill due next Friday and I'm terrified of getting hit with another $50 over-limit penalty.

As a senior on a fixed CPP income, the inflation this year has been absolutely brutal. I had to put my groceries and my hydro bill on my credit card just to survive the winter. This program might actually save my house.

Just completed my first full month on the program. My minimum payments used to be $850 combined across four cards. Now I pay one bill of $310. It feels like I can finally breathe again when I check my mail.

@CalgaryMom That sounds amazing. I'm so scared to pull the trigger because I don't want to mess up my mortgage renewal next year, but I'm drowning right now.

Just submitted my application. With the way the Bank of Canada is acting and groceries costing a fortune, I'm not waiting around to go bankrupt. Thanks for the article Dave!

Leave a comment